Anthony Butler is a senior advisor to a G20 central financial institution, Chainlink advisor, and former CTO of IBM Providers, Center East and Africa.

Central Financial institution Digital Currencies (CBDCs) proceed to be the topic of in depth analysis, experimentation, and evaluation globally as central banks think about what the way forward for cash might seem like and whether or not tokenised central financial institution cash ought to play a task in that future. This journey didn’t start, in fact, in 2024 however goes again a few years: with the CBDC idea evolving considerably from the earliest home experimentations via to cross-border experimentation and now, the emergent idea of a “finternet” that seeks to weave collectively the worlds of tokenised and non-tokenised property into a typical material.

Historical past of CBDCs

The primary CBDC experiments seem to return to 2014 when the Central Financial institution of Uruguay and China experimented with the e-Peso and e-CNY respectively. This was adopted by varied experiments similar to Canada’s Challenge Jasper, South Africa’s Khoka, Financial Authority of Singapore’s Ubin, and others. A few of these tasks sought to duplicate a type of digital money (i.e. retail CBDC) and others sought to duplicate the options and features of the RTGS (i.e. wholesale CBDC).

A lot of this early section of experimentation was centered on understanding this new know-how referred to as “blockchain” and whether or not there was a possible to create one thing in a regulated context that resembled the improvements that have been occurring throughout the crypto ecosystem with Bitcoin, Ethereum, and so forth.

These home experiments have been shortly adopted by multi-jurisdictional experiments the place the aperture was broadened to contemplate how CBDC may very well be used as devices of cross-border settlement. For instance, Hong Kong and Thailand’s Challenge Lionrock, Saudi Central Financial institution and UAE Central Financial institution’s Challenge Aber, Canada and Singapore’s integration of Jasper and Ubin (generally known as Jasper-Ubin), and Challenge Dunbar by which the BIS introduced collectively the central banks of Australia, Malaysia, Singapore and South Africa to check a number of CBDCs on a single shared platform. This latter venture demonstrated the efficacy of CBDCs for worldwide settlement and led to Challenge mBridge.

The drivers for cross-border experimentation have been totally different, with the first objective of those initiatives being to deal with inefficiencies in worldwide funds and remittances, which are sometimes gradual, pricey, and opaque. For instance, cross-border funds steadily take 3-5 days to clear and banks “proceed to be the most costly channel for sending remittances,” with a median value of 12.1% in response to the World Financial institution.

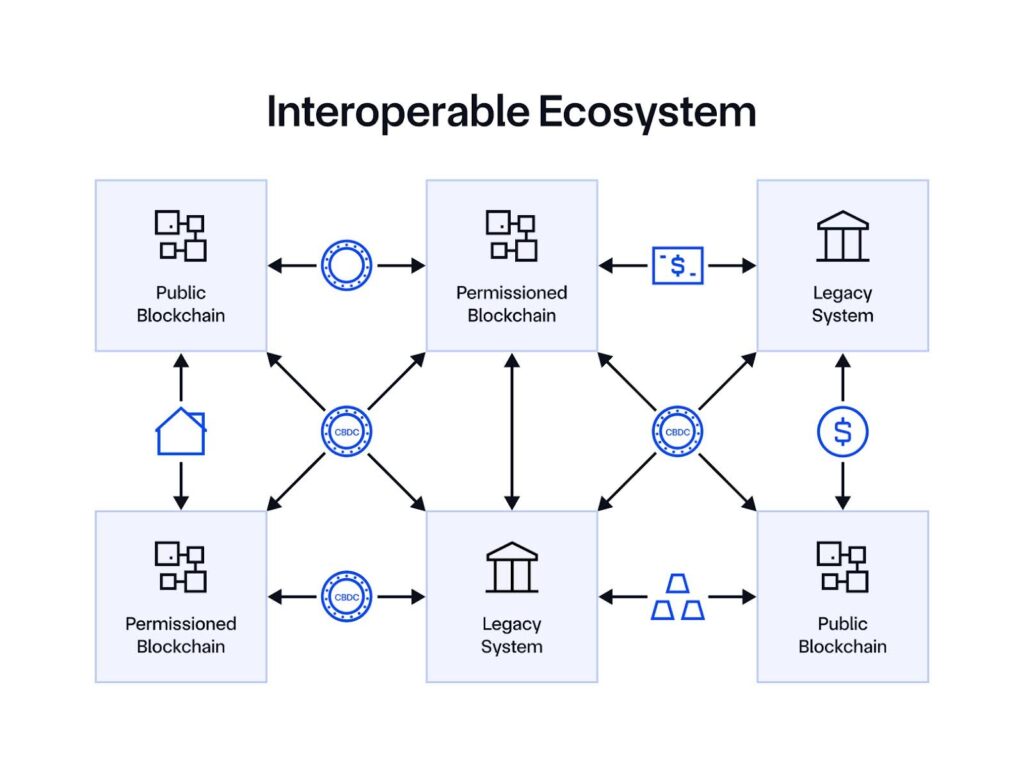

Present CBDC panorama

As we speak, there are nonetheless experiments being performed domestically and cross-border and there are a small variety of international locations which have, having seen tasks present vital effectivity, programmability, and composability benefits, decided to maneuver ahead with CBDCs. On the identical time, there at the moment are many examples of personal cash being tokenised too, such because the tokenised deposits which might be issued as tokenised claims towards business financial institution stability sheets. As with wCBDC, many of those are exploring cross-border situations too.

As we have a look at the evolution of this house and the efforts underway globally, it’s clear that it’s extremely unbelievable that the world will converge on a single blockchain platform that can span the globe and be the “common ledger” onto which all property and types of cash can be tokenised.

Key the reason why a singular “common ledger” is not going to be realised:

Not all international locations will transfer in direction of tokenisation on the identical time or identical tempo, so there can be a necessity for coexistence between the legacy and new methods for an prolonged period of time.

The selection of protocol or know-how to tokenize an asset, similar to permissioned or zero-knowledge primarily based chains for privateness, fast-finality options for funds, and public blockchains for decentralized safety, can be knowledgeable by the native jurisdictional necessities, the kind of asset being tokenised, the sorts of markets that the asset will have to be listed in, and a myriad of different purposeful and non-functional necessities that can lead in direction of a specific know-how. It’s possible, for instance, that totally different business banks might select to make use of totally different applied sciences for tokenised deposits, central banks might use different applied sciences for his or her CBDCs, property can be tokenised on quite a lot of different heterogenous networks primarily based on the place there’s demand and liquidity, and every system might want to interconnect with a myriad of different methods outdoors their jurisdiction similar to the assorted DLT and non-DLT primarily based messaging and cross-border funds methods.

The know-how is evolving shortly with scalability options that may help mass adoption and the obstacles to entry are being lowered such that it’s conceivable that, sooner or later sooner or later, instantiating a blockchain community can be analogous to the instantiation of a relational database in the present day; a scenario that can additional result in proliferation of networks.

There are already rising regional and different blocs by which totally different jurisdictions are coming collectively to construct their very own cross-border networks centered on a specific set of corridors or a specific area.

The tip result’s fragmentation, silos, and islands that, with out bridges, won’t be able to ship on the unique promise of blockchain.

We are able to discover synergies within the origins of the Web. Within the early days of the Web, there have been distinct networks that emerged to service totally different communities. There was ARPANET, CSNET, and NSFNET, for instance, and quite a lot of different networks that emerged in different components of the world. They didn’t have any strategy to talk with one another and have been, like the assorted DLT networks of in the present day, islands. On January 1st, 1983, this might change after they would undertake a typical “language” generally known as Switch Management Protocol/Internetwork Protocol or TCP/IP as it’s generally identified in the present day. It was the adoption of this common language that led to the start of the Web.

As we see the assorted DLT-based monetary networks following an analogous trajectory with islands rising, the query that have to be requested is how will we clear up the interoperability problem? What, one may ask, is the TCP/IP of the blockchain period that can enable the TradFi and DeFi worlds to interoperate but in addition, inside every, enable the assorted tokenised property, deposits, and CBDC platforms to speak to one another? As with the Web, it is just via the seamless integration of those networks that the true worth will be realised.

What would a TCP/IP of the blockchain world want to supply?

Firstly, this protocol ought to allow tokens—the “packets” of blockchain-based finance (onchain finance) containing worth and knowledge—to maneuver securely between networks, even heterogenous protocols, similar to public and permissioned. It ought to achieve this in a manner that ensures safety and the integrity of the system. For instance, it could clearly be problematic if some tokenised cash was moved from one community to a different but it continued to persist within the authentic community since this might allow “doubling spending” and would undermine the integrity of your complete system.

Second, sensible contracts ought to be capable of govern and orchestrate the motion of those tokens such that subtle settlement use instances will be executed, such because the switch of a CBDC from one community to a different happens solely contingent on the switch of a tokenised safety from one community to a different; or varied cost versus cost situations similar to exchanging CBDC on one community in a single forex for CBDC on one other community and in one other forex. As a way to help advanced operations cross-chain, the interoperability resolution have to be programmable, embedding each tokens and directions on what to do with these tokens in a single cross-chain transaction.

Thirdly, these tokens could also be created as representations of some bodily or “real-world property”, similar to a safety or actual property. On the time of being created, this hyperlink can be established and, because the token strikes between networks or cross-border, this hyperlink shouldn’t be damaged however ought to proceed to make sure that the token-holder has visibility and might believe within the linkage between the digital and bodily worlds via real-time proof of reserve verifications. Additional, as attributes of the bodily asset change over time, the token must also be up to date with offchain knowledge being injected into the token’s sensible contract to mirror these altering values.

Fourth, while TCP/IP was primarily based on the motion of packets with out consideration for what data was embedded in them, a TCP/IP of the blockchain world must bear in mind that a lot of what’s being moved is of actual monetary worth and is topic to a spread of advanced regulatory and different issues. There must be an acceptable oracle-based privateness and permissions mechanism that ensures the safety of the system whereas additionally supporting compliance with varied rules, enabling establishments to use predefined controls and limits throughout transactional exercise, together with insurance policies round id, AML/KYC, authorized necessities, organizational restrictions, and extra.

Fifth, there must be a recognition that so-called legacy methods might want to co-exist and synchronize with the brand new methods and subsequently the protocol ought to allow the seamless motion of worth and knowledge between these legacy worlds and the tokenised world—and vice versa.

Lastly, as CBDCs or different tokenized property transfer throughout chains via their lifecycle, they have to be frequently up to date with key value, reserves possession, compliance, and different knowledge, no matter which setting they’re transferred to. This might allow the creation of a unified golden file—a single supply of fact that every one stakeholders can learn from.

out of Canada")